Collier planners back new village in rural area near Lee County line

Laura Layden | Fort Myers News-Press & Naples Daily News

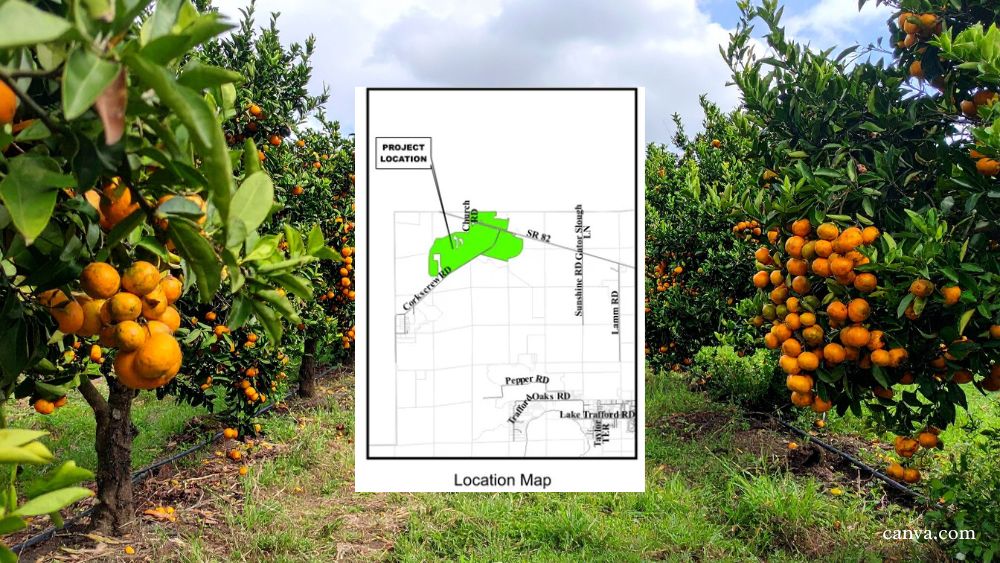

A longtime citrus grower’s plans to build a new village in rural Collier County have cleared another regulatory hurdle.

On March 19, the Collier County Planning Commission voted unanimously in favor of allowing Fort Myers-based Alico Inc. to create a stewardship receiving area on land where the company has grown and harvested oranges for decades.

The designation as a receiving area would allow Alico to develop a more than 1,400-acre village, known as Corkscrew Grove East.

The planning commission, sitting as the local planning agency and the Environmental Advisory Council, voted 4-0 to recommend approval to county commissioners, who will make the final decision.

The proposed village would have up to 4,502 residences and nearly 240,000 square feet of commercial uses, including retail shops, restaurants and medical offices, along with at least 45,020 square feet of civic spaces, which could be used for schools, churches and emergency services.

The village would include affordable housing.

Read the full article on naplesnews.com.

Are you seeking a home in the Bonita Springs – Naples, Florida area? Contact David at David@DavidFlorida.com or 239-285-1086.